Week ahead: US data and Powell in the spotlight

Where we were

‘Wait and see’ seems to be the dominant sentiment for both US President Donald Trump and the US Federal Reserve (Fed).

The escalating Israel-Iran conflict saw a series of back-and-forth assaults from both sides last week, alongside the possibility of US involvement. Reports emerged that Trump had authorised a military strike against Iran but had yet to issue a final order. This was quickly eclipsed by the President announcing a wait-and-see policy regarding Iran, leaving the door ajar for another ‘two weeks’ in the hope of a negotiation. The ideal scenario here, of course, would be a diplomatic resolution; however, tensions remain high.

A continued concern in the Middle East is the potential closure of the Strait of Hormuz – an important shipping lane that facilitates approximately 20% of global Oil. Although I do not believe it will come to this, such a closure would lead to economic repercussions, likely necessitate international intervention, and further increase Oil prices.

In terms of the Fed’s rate announcement last week, it was largely a snoozer and one of the most lacklustre market reactions I have seen in a while. As anticipated, the funds target rate was left unchanged at 4.25%-4.50%, and forward guidance largely echoed a similar tone: a cautious, ‘wait-and-see’ stance, with no urgency to reduce policy at this point, despite pressure from Trump. Fed Chair Jerome Powell also reiterated that the central bank remains ‘well-positioned’ to wait for further clarity.

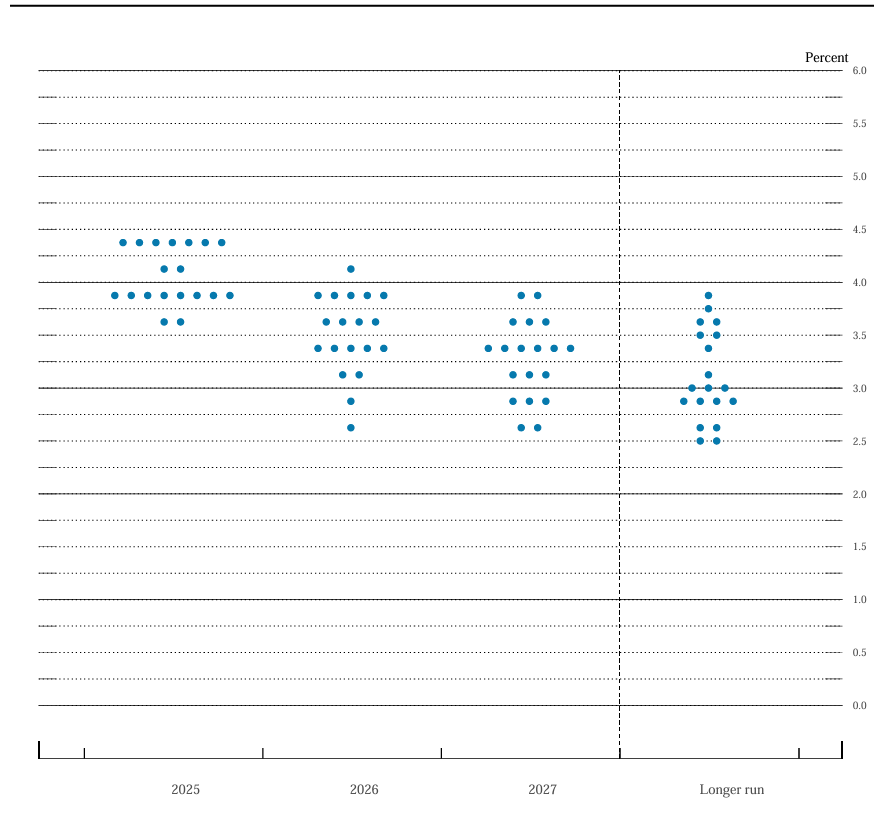

Regarding the Summary of Economic Projections, the central bank continues to expect two rate cuts this year, though one less in 2026 and 2027. What was interesting was that, although the median ‘dots’ did not change, the dots did move and indicated an increasing divide among Fed members. As you can see from the Fed’s dot-plot below, seven members of the Committee call for rates to remain unchanged, which is an increase from the March projections. On one hand, those advocating for rate cuts are concerned about the growth implications of elevated rates, while on the other hand, those in favour of maintaining rates unchanged are worried about inflation. However, I will be taking this chart with a rather large pinch of salt, given that Fed members face an incredible amount of uncertainty at the moment, and forecasts will likely present a different picture later in the year.

Where we were

‘Wait and see’ seems to be the dominant sentiment for both US President Donald Trump and the US Federal Reserve (Fed).

The escalating Israel-Iran conflict saw a series of back-and-forth assaults from both sides last week, alongside the possibility of US involvement. Reports emerged that Trump had authorised a military strike against Iran but had yet to issue a final order. This was quickly eclipsed by the President announcing a wait-and-see policy regarding Iran, leaving the door ajar for another ‘two weeks’ in the hope of a negotiation. The ideal scenario here, of course, would be a diplomatic resolution; however, tensions remain high.

A continued concern in the Middle East is the potential closure of the Strait of Hormuz – an important shipping lane that facilitates approximately 20% of global Oil. Although I do not believe it will come to this, such a closure would lead to economic repercussions, likely necessitate international intervention, and further increase Oil prices.

In terms of the Fed’s rate announcement last week, it was largely a snoozer and one of the most lacklustre market reactions I have seen in a while. As anticipated, the funds target rate was left unchanged at 4.25%-4.50%, and forward guidance largely echoed a similar tone: a cautious, ‘wait-and-see’ stance, with no urgency to reduce policy at this point, despite pressure from Trump. Fed Chair Jerome Powell also reiterated that the central bank remains ‘well-positioned’ to wait for further clarity.

Regarding the Summary of Economic Projections, the central bank continues to expect two rate cuts this year, though one less in 2026 and 2027. What was interesting was that, although the median ‘dots’ did not change, the dots did move and indicated an increasing divide among Fed members. As you can see from the Fed’s dot-plot below, seven members of the Committee call for rates to remain unchanged, which is an increase from the March projections. On one hand, those advocating for rate cuts are concerned about the growth implications of elevated rates, while on the other hand, those in favour of maintaining rates unchanged are worried about inflation. However, I will be taking this chart with a rather large pinch of salt, given that Fed members face an incredible amount of uncertainty at the moment, and forecasts will likely present a different picture later in the year.

Unsurprisingly, Powell noted that the meeting’s forecasts are subject to uncertainty, adding that ‘uncertainty is unusually elevated’ at this time, referring to trade policy and geopolitical risks out of the Middle East. There is not enough conviction among Fed members, given the current levels of uncertainty. However, the policy path is consistent with market pricing, which suggests that September’s meeting could be the date to watch for the first 25-basis point (bp) cut.

While Powell refrained from explicitly using the term ‘stagflation’ in his press conference, it would be difficult to deny that the ‘risks’ of stagflation have increased based on these updated economic projections. PCE (Personal Consumption Expenditures) inflation was revised upwards in all years, rising to 3.0% from 2.7% for 2025, to 2.4% from 2.2% for 2026, and to 2.1% from 2.0% for 2027. Growth was also downgraded, with unemployment projections elevated across all years (to 4.5%, 4.5%, and 4.4% for 2025, 2026, and 2027, respectively).

In addition to the above, several other central banks claimed some of the limelight last week:

- The Bank of Japan maintained its policy rate at 0.50%, which was expected, and outlined a measured approach to unwinding its bond-buying programme. The central bank also reiterated its current plan to reduce monthly Japanese government bond (JGB) purchases by ¥400 billion per quarter to ¥3 trillion until March 2026.

- The Bank of England (BoE) maintained the bank rate at 4.25%. This, coupled with the central bank’s ongoing commitment to a ‘careful and gradual’ approach, was expected. What dominated the airwaves following this meeting was the Monetary Policy Committee (MPC) vote, which took on a slightly more dovish tilt with a 6-3 vote in favour of a hold, rather than the 7-2 vote forecasted. Swati Dhingra and Alan Taylor (external members known for their dovish stance) were expectedly among those advocating for a rate cut, while Deputy Governor Dave Ramsden also supported this position. For reference, the BoE has nine members: the Governor, three Deputy Governors, the Chief Economist, and four external members. Markets are now pricing in a 60% probability of a 25-bp cut at August’s meeting. A lot can happen before then, and August is far from certain. BoE Governor Andrew Bailey commented that he ‘expects that the path of interest rates will continue to be gradually downwards’. Still, he cautioned that he was not providing a ‘prediction for August by saying that’.

- The Swiss National Bank (SNB) reduced its policy rate by 25 bps to 0.00% from 0.25% to combat lagging inflationary pressures and strength in the Swiss franc (CHF). SNB Chair Martin Schlegel indicated the central bank would not easily resort to negative rates, considering the impact on savers and pension funds. However, he didn’t rule it out if global trade turmoil persists.

Where we are

With no major central bank decisions due, the final full week of June will be focussed on geopolitical developments, upcoming data, and Powell’s testimony.

On the data front, Friday brings US PCE Price Index numbers, which is the Fed’s preferred inflation gauge. Year-on-year (YY) PCE data are expected to have risen by 2.3% in May YY at the headline level, up from 2.1% in April, with the YY core measure also forecast to have ticked higher to 2.6% from 2.5%. A rise in inflation would be consistent with the general tariff-induced inflation. Nevertheless, this is likely to become more apparent in subsequent months of data. Should we see higher-than-expected inflation figures this week, this will help reinforce the Fed’s wait-and-see stance and likely underpin a bid in the US dollar.

Overall, I would say that inflation is currently under control, and the Fed has no reason to adjust its policy at this point, which is something I expect Powell to reiterate to Congress this week. Powell will address the House on Tuesday and the Senate Banking Committee on Wednesday. As I noted above, I expect Powell to echo a similar sentiment to what we have already heard and emphasise that the Fed is data-dependent, which will guide the timing of rate adjustments.

Additional data to be aware of this week:

- Monday kicks off with the forward-looking flash manufacturing and services PMIs (Purchasing Managers’ Indices) for June, coming from the Eurozone, the UK, and the US.

- The focus shifts to North America on Tuesday, with the release of Canadian CPI (Consumer Price Index) inflation data for May.

- Tuesday also welcomes the US Conference Board’s consumer confidence survey for June.

- As the trading week draws to a close, the final estimate for US Q1 25 GDP (Gross Domestic Product) growth will offer a comprehensive and updated picture of the economy’s performance during the first three months of the year.

Charts created using TradingView

Written by FP Markets Chief Market Analyst Aaron Hill

Unsurprisingly, Powell noted that the meeting’s forecasts are subject to uncertainty, adding that ‘uncertainty is unusually elevated’ at this time, referring to trade policy and geopolitical risks out of the Middle East. There is not enough conviction among Fed members, given the current levels of uncertainty. However, the policy path is consistent with market pricing, which suggests that September’s meeting could be the date to watch for the first 25-basis point (bp) cut.

While Powell refrained from explicitly using the term ‘stagflation’ in his press conference, it would be difficult to deny that the ‘risks’ of stagflation have increased based on these updated economic projections. PCE (Personal Consumption Expenditures) inflation was revised upwards in all years, rising to 3.0% from 2.7% for 2025, to 2.4% from 2.2% for 2026, and to 2.1% from 2.0% for 2027. Growth was also downgraded, with unemployment projections elevated across all years (to 4.5%, 4.5%, and 4.4% for 2025, 2026, and 2027, respectively).

In addition to the above, several other central banks claimed some of the limelight last week:

- The Bank of Japan maintained its policy rate at 0.50%, which was expected, and outlined a measured approach to unwinding its bond-buying programme. The central bank also reiterated its current plan to reduce monthly Japanese government bond (JGB) purchases by ¥400 billion per quarter to ¥3 trillion until March 2026.

- The Bank of England (BoE) maintained the bank rate at 4.25%. This, coupled with the central bank’s ongoing commitment to a ‘careful and gradual’ approach, was expected. What dominated the airwaves following this meeting was the Monetary Policy Committee (MPC) vote, which took on a slightly more dovish tilt with a 6-3 vote in favour of a hold, rather than the 7-2 vote forecasted. Swati Dhingra and Alan Taylor (external members known for their dovish stance) were expectedly among those advocating for a rate cut, while Deputy Governor Dave Ramsden also supported this position. For reference, the BoE has nine members: the Governor, three Deputy Governors, the Chief Economist, and four external members. Markets are now pricing in a 60% probability of a 25-bp cut at August’s meeting. A lot can happen before then, and August is far from certain. BoE Governor Andrew Bailey commented that he ‘expects that the path of interest rates will continue to be gradually downwards’. Still, he cautioned that he was not providing a ‘prediction for August by saying that’.

- The Swiss National Bank (SNB) reduced its policy rate by 25 bps to 0.00% from 0.25% to combat lagging inflationary pressures and strength in the Swiss franc (CHF). SNB Chair Martin Schlegel indicated the central bank would not easily resort to negative rates, considering the impact on savers and pension funds. However, he didn’t rule it out if global trade turmoil persists.

Where we are

With no major central bank decisions due, the final full week of June will be focussed on geopolitical developments, upcoming data, and Powell’s testimony.

On the data front, Friday brings US PCE Price Index numbers, which is the Fed’s preferred inflation gauge. Year-on-year (YY) PCE data are expected to have risen by 2.3% in May YY at the headline level, up from 2.1% in April, with the YY core measure also forecast to have ticked higher to 2.6% from 2.5%. A rise in inflation would be consistent with the general tariff-induced inflation. Nevertheless, this is likely to become more apparent in subsequent months of data. Should we see higher-than-expected inflation figures this week, this will help reinforce the Fed’s wait-and-see stance and likely underpin a bid in the US dollar.

Overall, I would say that inflation is currently under control, and the Fed has no reason to adjust its policy at this point, which is something I expect Powell to reiterate to Congress this week. Powell will address the House on Tuesday and the Senate Banking Committee on Wednesday. As I noted above, I expect Powell to echo a similar sentiment to what we have already heard and emphasise that the Fed is data-dependent, which will guide the timing of rate adjustments.

Additional data to be aware of this week:

- Monday kicks off with the forward-looking flash manufacturing and services PMIs (Purchasing Managers’ Indices) for June, coming from the Eurozone, the UK, and the US.

- The focus shifts to North America on Tuesday, with the release of Canadian CPI (Consumer Price Index) inflation data for May.

- Tuesday also welcomes the US Conference Board’s consumer confidence survey for June.

- As the trading week draws to a close, the final estimate for US Q1 25 GDP (Gross Domestic Product) growth will offer a comprehensive and updated picture of the economy’s performance during the first three months of the year.

Charts created using TradingView

Written by FP Markets Chief Market Analyst Aaron HillPublication date:

2025-06-23 11:46:24 (GMT)